- News

- Business News

- India Business News

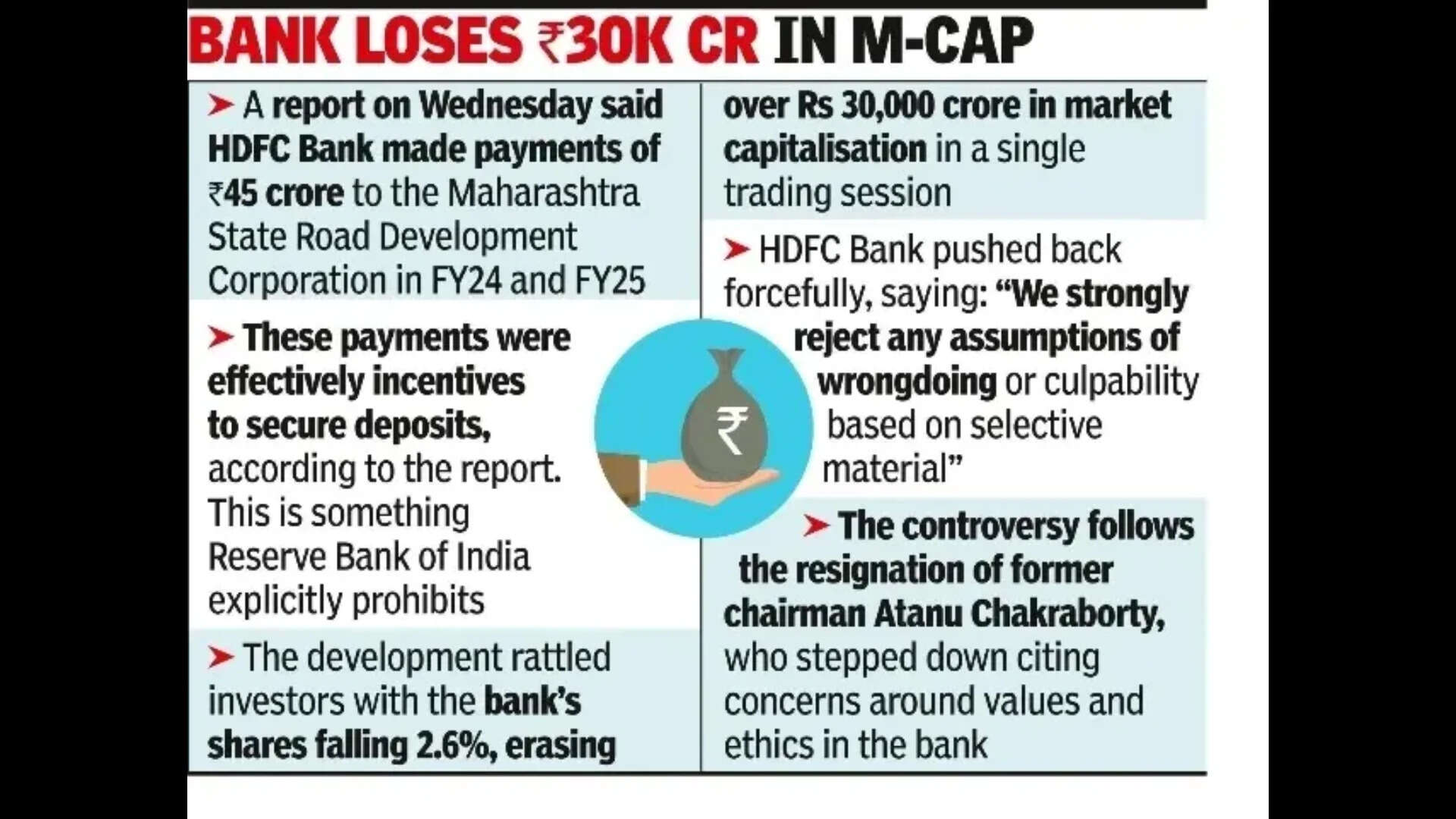

- HDFC shares fall 2.6% over 'extra payout' report

Trending

HDFC shares fall 2.6% over 'extra payout' report

Representative image

End of Article

Follow Us On Social Media

Hot Picks

Top Trending

Tired of too many ads?go ad free now

Trending Stories

In Business

Entire Website

- Hyundai to hike car prices from June 1

- SBI chief flags inflation, growth worries

- 2025-26 foodgrain production estimated at record 376 MT

- Three months of Hormuz chaos: Oil prices ease amid hopes of US-Iran peace deal

- Cabinet okays Rs 25k crore scheme to modernise PDS scheme

- AI, AI Express, IndiGo to slash 250 domestic flights a day

- Gaming companies face Rs 2.5 lakh crore hit as SC upholds GST

- First make 50 cities completely clean: PM to urban affairs ministry, states

- Stock market holiday on Bakri Id: Are BSE, NSE closed for trading on May 28?

- Sensex bleeding, gold volatile amid US-Iran war: Time to opt for good old FDs? Pros & cons of fixed income assets

- IPL 2026 Orange Cap: Vaibhav Sooryavanshi reclaims top spot after 97-run knock vs SRH

- IPL 2026: Vaibhav Sooryavanshi scripts history, becomes first batter to...

- Several feared dead after boat carrying 14 overturns in Ganga near Patna; 2 bodies recovered

- WWE star Drew McIntyre drops unexpected IPL tribute to Vaibhav Sooryavanshi before Rajasthan Royals playoff clash

- 'New six machine': Chris Gayle makes Vaibhav Sooryavanshi admission after 15-year-old breaks his IPL record

- "Doubt she’s got anything left": Taylor Swift goes through major personal loss ahead of her wedding with Travis Kelce

- Cristiano Ronaldo-backed YouTube platform to stream all 104 FIFA World Cup matches in 4K to millions for free

- MLB trade rumors: Diamondbacks star Ketel Marte emerges as Yankees’ biggest trade target before August deadline

- Emma Raducanu net worth in 2026: Inside the British tennis star’s earnings, endorsements and investments

- Norway Chess: R Praggnanandhaa shocks World No. 1 Magnus Carlsen in classical; 3rd straight Armageddon win for Divya Deshmukh

Financial calculators

Explore Every Corner

Across The Globe

SRH vs RR HighlightsIran War NewsNBA Trade RumorIPL Orange CapNorway ChessVaibhav SooryavanshiMLB Trade RumorsSebastian CossaTravis KelceTiger WoodsPinarayi VijayanBob Horner DeathKendrick PerkinsLionel Messi and Antonela Roccuzzo Net WorthJosh Jacobs GirlfriendEmma Raducanu Net WorthRoger FedererChris GayleConor McGregorGlenn PhillipsCarter HartRafael NadalLionel MessiNHL Trade RumorsRoger FedererIlia Topuria Net WorthMadison BeerJosh JacobsDianna RussiniKim Kardashian Ex Boyfriend Hospitalized

Hot on the Web

Priya KapurRanveer SinghEid-ul-Adha WishesAnik DuttaRanveer Singh ControversyRam CharanImtiaz AliWhen is BakridFarhan AkhtarEid Mubarak WishesBakrid WishesDrishyam 3 Box Office CollectionJohn McclainDhurandhar Television PremiereImtiaz AliPam BondiChand Mera Dil Box Office CollectionMeenakshi SeshadriAishwarya Rai BachchanSalman KhanKaruppu Box Office CollectionVirat KohliAshoke PanditZubeen GargKangana RanautAR RahmanBaby NamesDhurandhar 2 Box Office CollectionPati Patni Aur Woh Do Box Office CollectionHoroscope TodayHarpy Eagle Vs Philippine EagleVenomous Vs Non Venomous SnakesUS Powerball LotteryHighest Anaconda PopulationWorld Highest Paid AthletesINS KolkataNyt ConnectionsTwisha Sharma Death CaseRanveer Singh BannedChina New Humanoid RobotS 400Captions For Instagram Posts

Trending Topics

RR VS SRH IPL MatchShreyas IyerPSSSB Excise Inspector Admit CardLakshmir Bhandar SchemeRiyan ParagREET Mains Result 2026UK HeatwaveVaibhav SooryavanshiCBSE re-evaluationMLA Jagroop Singh GillCM Pinarayi VijayanDU girl 'rape' caseBank holiday todaySiddaramaiahSuvendu AdhikariDelhi temperatureAbhishek BanerjeeTwisha SharmaKolkata Messi statueEbola bengaluruKarnataka CM newsSiddaramaiahIndian Navy Piracy AttackGolders Green FireEbola AlertDelhi Smart Ration DistributionPakistan Baseless RemarksDelhi Illegal Animal SacrificeKasauli Forest FireIPL Purple CapCloudflare LayoffApple Google Seek CourtApple Theft DetectionJeff BezosAI Guided Cruise Missiles007 First lightAndrew MacdonaldTim CookGarena Free Fire MAX Redeem CodesPeroxide CodesGenshin Impact Codes

Popular Categories

HeadlinesSports NewsBusiness NewsIndia NewsWorld NewsInternational SportsHealthIndian TV ShowsTechnologyTravelEtimesAstrologyDeorhiAutoTechnology NewsGold Rate TodayWeather TodaySilver Price TodayDelhi Weather TodayPetrol Price TodayDiesel Price TodayCNG Price TodayLPG Price TodayPetrol Price MumbaiDelhi AQIIs Bank Open TodayMumbai AQI TodayIs Bank Open TomorrowPublic Holidays in MayBank Holidays in May

Trending Videos

Trump Defends ‘Incredible’ Tulsi Gabbard After Resignation Triggers Brutal Political BacklashUAE ‘Sleepwalks’ Into War With Iran? SECRET Netanyahu, Mossad Meetings Drag MBZ Into ‘Israel’s Mess’ON CAM: Trump PANICS Over Xi-Putin’s ‘Iran Nuclear Plan’, Reveals Who Will Takeover Iran’s Uranium'Hang Him By Neck Till Death': Ex-US Marine's Blistering Attack On Trump Amid Iran War‘We Have To Bomb…’: Trump Goes Nuclear On Oman For ‘Ditching US’, ‘Siding With Iran’ On HormuzBig Reveal: America’s Soldier Casualties ‘Surge’ Amid Fresh Iran Clash; Pentagon ‘Still Hiding…’Trump ‘Hands’ Texas To Democrats? GOP’s ‘Public Meltdown’ After Ken Paxton’s Shock Primary Win'Lot Of Missiles But...': Hegseth Admits Iran Still Missile-Ready After Weeks Of BombardmentIPL 2026 Eliminator: James Franklin hails Vaibhav Sooryavanshi despite SRH’s heartbreakIPL 2026: Dhruv Jurel reveals what makes Vaibhav Sooryavanshi extra specialKimmel Blasts Trump’s 'Perfect Health' Remark; Late-Night Host Questions Cognitive Test BraggingFrom Dominance to Damage Control? Iran 'Forces US To Take Sudden U-Turn' Amid Talks TussleU.S. Caught In Crisis Web as China Emerges as Unexpected Power Broker'No Longer in Control…': Russia-Iran 'Checkmate' Forces Trump Into Global Damage Control ModeDonald Trump Mocked After Memorial Day Appearance; Assistant Faces Backlash Over Viral PhotoExplained: What Is The CMRL-Exalogic Case Linked To ED Raids On Ex-Kerala CM Pinarayi VijayanHezbollah's Killer Drones Pierce Through Northern Israel In CHILLING Video | WatchRoyal Wedding Thrown Into Chaos After Fresh Andrew Allegations Spark New Family Crisis

Latest News

Hazaribag man drowns while fishing in lake"Behen Darr Gayi!": Fans relive ‘Bhagam Bhag’ era after watching Akshay Kumar's 'Bhooth Bangla' trailerMBOSE HSLC result 2026 to release tomorrow: Check details hereIran war risk: JPMorgan CEO Jamie Dimon warns of oil shocks, sticky inflation and higher interest ratesMake your clutch last longer with these easy driving tips“Three-against-one situation”: El Rubius opens up on being “targeted” in MrBeast’s viral $1M challengeBihar BTSC lab assistant notification released for 1091 posts at btsc.bihar.gov.in; apply hereIPL craze costs techie Rs 1.46 lakh in fake RCB vs CSK ticket scamRaising “robot-proof” kids: Why creativity and curiosity matter more than everInside ‘Satguru Sharan’: Exploring Saif Ali Khan and Kareena Kapoor Khan’s Rs 100 crore Bandra homeHow selling Alaska in 1867 was a costly mistake for Russia'Hera Pheri 3 is coming': Paresh Rawal dismisses delay reports and reveals he will 'start shooting soon'US-Iran War: A daring rescue Hollywood blockbuster is on its way. Till then, pick your favourite from these 10 films on bringing someone home against all oddsKolkata team unveils fan mural at Rash Behari Avenue, celebrating city’s first loveHow US spread a lie to rescue a pilot of a jet shot down in IranNetflix unveils ‘VOID’, an AI model that can change a movie plotAI data centers are causing 'stress' not just to tech companies, but also private insurers"Trans women are.....": Clavicular’s viral moment with trans women sparks fresh conversation on internet culture

Copyright © 2026 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service